Klodian Tomorri

The Albanian insurance market has been showing a worrying trend of deterioration in the last two years, as data shows a significant increase in unpaid claims. According to official statistics from the Financial Supervisory Authority, at the end of September the number of pending claims for non-life insurance reached 12,206, reaching the levels of the year after the earthquake and the Covid one.

The number of pending claims includes claims in the assessment process, those approved but not paid by insurance companies, claims in court proceedings, etc. In short, they are accidents or damage events that have occurred, for which the injured parties have not yet received compensation money from the insurance companies.

This indicator is the most important indicator, showing how correct insurance companies are in settling claims without burdening injured citizens with bureaucracy, counterclaims, and legal proceedings, which in Albania last for years.

However, the number of pending claims is only one of the indicators that shows the worrying trend. There are two other indicators that confirm the same trend.

The first is the total value of outstanding claims. According to the AFSA, at the end of the 9 months, the total value of outstanding claims for non-life companies was 70 million euros. This figure is almost equal to the total value of claims that the Albanian market pays annually for non-life insurance.

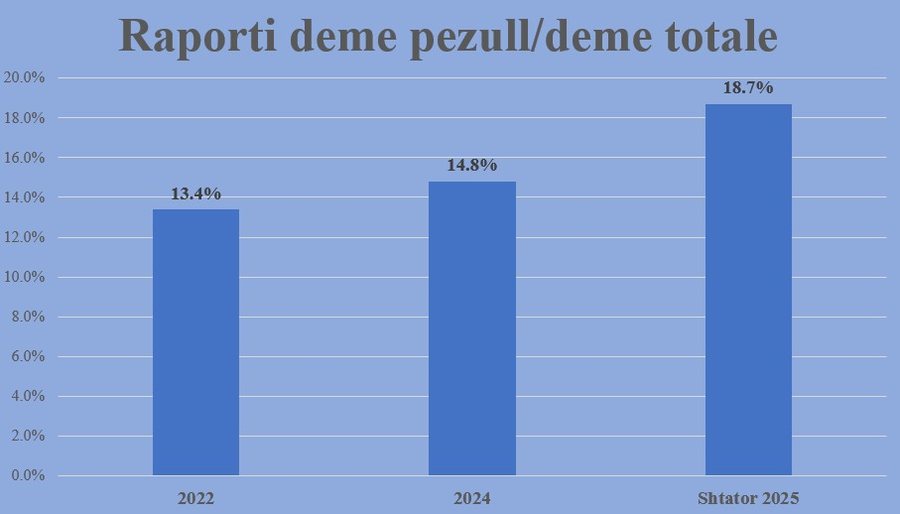

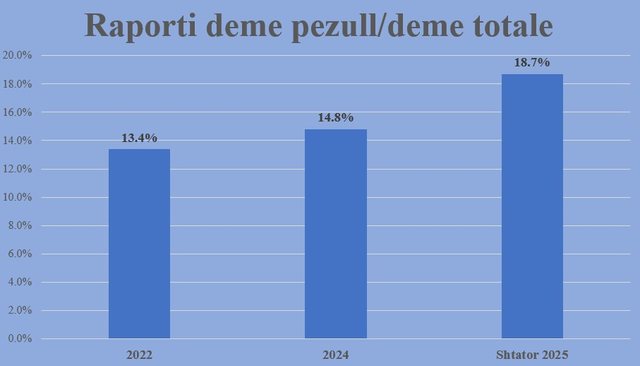

While the second indicator is the ratio of pending claims to the total number of claims. According to AFSA data, in 2022 this ratio dropped to 13.4 percent. But at the end of last year the ratio increased to 14.8 percent, while in September this year it jumped to 18.7 percent.

Only one company pays correctly

But the above figures are the average for the entire market. Detailed data shows a clearer picture of which Albanian insurance companies are the ones that do not pay but endlessly bring injured citizens around.

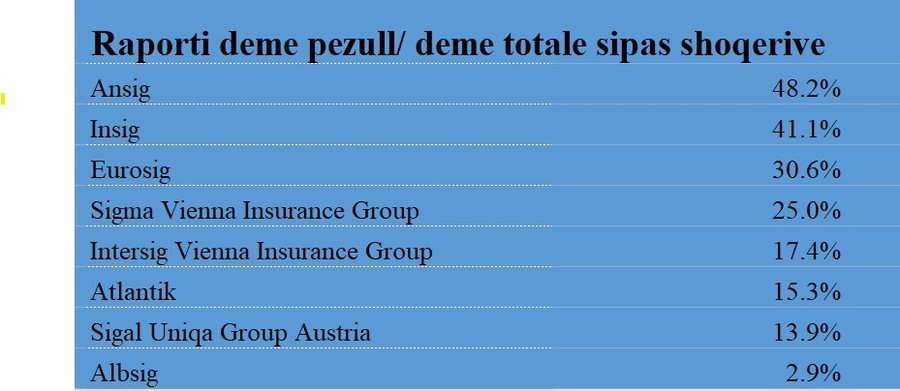

According to the data, Ansig, the insurance company owned by Piro and Llazi Angjeli, is at the top. For the period January-September, this company has paid a total of 1949 claims. But for the same period, according to the AMF, Ansig has 1814 pending claims, unpaid with a ratio of pending claims to total claims of 48.2 percent. This means that for every two claims that occurred, Ansig has paid only one claim.

In second and third place, among companies that are not correct in paying claims, are two companies owned by businessman Kadri Morina. Insig and Eurosig have a ratio of 41.1 percent and 30.6 percent, respectively, of pending claims over total claims.

The list is followed by Sigma Vienna Insurance Group with 25 percent, Intersig 17.4 percent and Atlantik with 15.3 percent. The largest insurance company in the country, Sigal, also has a double-digit ratio of outstanding claims to total claims.

According to the AFSA, for the period January-September of this year, Sigal has paid a total of 15,101 claims and for the same period it results in having 2,442 pending unpaid claims with a ratio of almost 14 percent of pending claims over total claims.

The only honest company in the Albanian insurance market, which pays on time and has a pending claims ratio similar to European insurance companies, is Albsig.

The Albsig company paid 12,871 claims for the period January-September and has only 388 pending claims. This makes the ratio of pending claims to total claims at Albsig, according to the AMF, only 2.9 percent, an indicator that proves that the company quickly settles all claims.

A solid market

The problem with the Albanian insurance market is its rigidity and the regulator's inability to punish companies that are not correct in paying claims.

In a normal market, with choices, citizens would choose companies that are fair to insure their vehicles, properties, and any other assets. This would encourage unfair companies to pay claims on time, or lead to their exit from the market.

But the Albanian insurance industry functions as a cartel with a divided market, where each company maintains the same market weight, regardless of whether they pay or not.

If this is added to the fact that the AFSA is powerless or compromised to enforce the rules, then the market is completely rigid and citizens are caught in the trap that their insurance policy can be used by companies that do not pay.

These developments also raise a big question about the insurance industry: Why should insurance companies exist that do not pay out in the market and have outstanding claims ratios of up to 50 percent?

Editorial